50 absolute ave unit 3806 Mississauga Ontario L4Z0A8

Register Education Saving Plan

Aim:

The aim of RESP is to save money in a tax shelter for a beneficiary’s post-secondary studies, generally that of a child.

Contribution Ceiling

- To make the most of the RESP’s tax advantages, the federal government has set a cumulative lifetime maximum of $50,000 per beneficiary.

- The contribution ceiling is “per beneficiary” for all RESP contracts in his/her name and not “per subscriber”.

Types of RESPs

There are three types of RESPs you can consider: individual plans, family plans, and group plans.

- Individual plans are ideal for single children or children outside the family.

- These plans have a single beneficiary and a lifetime contribution limit of $50,000.

- There is no minimum initial contribution for individual plans.

- The interesting thing about these plans is that you can open individual plans for adults as well.

- However, adult beneficiaries are not eligible for the Canada Education Savings Grant, which is only available until the beneficiary turns 17.

- Family planning can be started for several children in a family. However, all beneficiaries must be related to the subscriber.

- The income can be divided between beneficiaries and each child can benefit from government subsidies.

- If one of the children decides not to use their share of the RESP, the funds can be allocated to the other beneficiaries of the plan.

- The family plan has a lifetime contribution limit of $50,000 per beneficiary. As with individual plans, there is no minimum deposit when opening a plan.

- Group plans, also known as scholarship plans, are offered by group plan vendors.

- The seller is also the executor of the plan and takes all investment decisions.

- Group plans usually have a minimum initial deposit and tend to have higher fees.

- Group programs also require buyers to commit to making regular donations over a period of time.

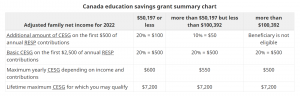

The Canada Education Savings Grant (CESG)

- The federal government created the Canada Education Savings Grant (CESG) program in 1998 to encourage parents to invest in their children’s post-secondary education.

- The CESG is equivalent to 20% of the first $2,500 in contributions made per beneficiary aged 17 years and under. It is calculated and paid into the plan on a monthly basis.

- The CESG ceiling is $7,200 per beneficiary.

- It is the plan promoter, in this case the Company, that applies for the CESG on the subscriber’s behalf. However, to be considered eligible, the beneficiary must have a social insurance number (SIN) and be a Canadian resident.

- Certain restrictions apply to beneficiaries 16 and 17 years of age.

- On January 1, 2005, the federal government increased the CESG amount available to low-income families. As a result, grants can now be as much as 40% of the first $500 in contributions. Children born on or after January 1, 2004, may also be eligible for a Canada Learning Bond, the maximum amount of which is $2,000 over a 15-year period.

Beneficiary Eligibility Criteria

- Individual Plans: Anyone with a SIN can be the beneficiary of an individual plan. However, there can only be one beneficiary per plan.

- Family Plans (My Education+ only): The beneficiary must be related to the subscriber by blood or adoption and have a SIN. There can be one or more beneficiaries per plan.

Withdrawals from an RESP

RESPs mature a maximum of 35 years after they’ve been established. However, no further contributions can be made after the contract’s 31st year.

Educational Assistance Payments (EAPs):

- Educational assistance payments include any payments, other than contribution reimbursements, that are made to a beneficiary who is enrolled in an eligible post-secondary program.

- The subscriber can decide the amount and frequency of EAPs once the beneficiary begins post-secondary studies.

- EAPs are intended to help pay for tuition fees and other education-related expenses and costs, including lodging, school supplies, food, transportation, etc. EAPs can be spread out over several years of study and are included in the student’s total annual income.

Accumulated Income Payments:

- Accumulated income payments (AIPs) correspond to the distribution of investment income earned on RESP contributions and the CESG.

- It is not an educational assistance payment or a contribution refund.

- In the event that AIPs cannot be transferred to an RRSP they must be included in the subscriber’s current income and will also be subject to an additional 20% tax.

Withdrawal of Contributions:

- Subscribers can withdraw their contributions at any time without any impact on their taxes. However, certain fees may apply and will vary according to the type of education savings plan chosen.

- If withdrawals are made before the beneficiary has begun post-secondary studies, the amount of the CESG attributable to the withdrawal must be reimbursed. Furthermore, such withdrawals could result in restrictions on the amount of any future CESGs.

Designating a New Beneficiary:

- If the beneficiary does not attend a post-secondary institution, the subscriber may either name another beneficiary or be obligated to refund the CESG.

- In a family plan, EAPs can be made arbitrarily to each or all of the designated beneficiaries, up to a maximum of $7,200 per beneficiary.

Transfer of Accumulated Earnings into Your RRSP:

- If none of the beneficiaries pursue a post-secondary education considered admissible under the plan, the youngest beneficiary is over the age of 21 and the plan has been in existence for over 10 years, it is possible, under certain conditions, to transfer the earnings generated by the RESP to the RRSP of either the subscriber or his/her spouse, up to a maximum of $50,000.

- Fees Certain fees may apply and will vary according to the type of education savings plan chosen.

Fees:

- Certain fees may apply and will vary according to the type of education savings plan chosen.

Advantages of Each Type of plan:

- Individual Plans: Individual plans offer great flexibility with regards to beneficiary designation.

- Family Plans (My Education+ only): Family plans offer great flexibility in terms of the distribution of EAPs. Payments can be made to only one beneficiary or divided equally among several beneficiaries designated in the plan.